Access information in your language

If English is not your first language, interpreter services are available to help you.

Absentee corporations

Companies based overseas may pay a surcharge.

Key information

If you are an absentee owner, an absentee owner surcharge applies to your land tax.

An absentee owner includes an absentee corporation.

An absentee corporation is a corporation:

- incorporated outside Australia, or

- in which an absentee person has an absentee controlling interest.

Absentee controlling interest

An absentee person has an absentee controlling interest if – either alone or with another absentee person – they:

- hold more than 50% of the corporation’s shares

- can control how the corporation’s board is composed

- can cast more than 50% of the maximum number of votes at the corporation’s general meeting.

The absentee person with a controlling interest can be an absentee corporation, a trustee of an absentee trust or an absentee individual.

To work out if one or more absentee persons have a controlling interest in a corporation, you must look at all absentee persons who can exercise a controlling interest over the corporation.

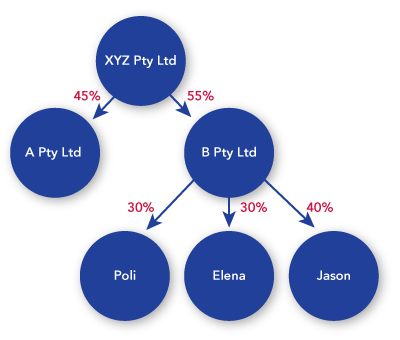

Example - controlling interest

XYZ Pty Ltd is a company that is incorporated in Australia and owns taxable land in Victoria.

XYZ Pty Ltd has 2 shareholders:

- A Pty Ltd, which holds 45% of the shares

- B Pty Ltd, which holds 55% of the shares.

Both A Pty Ltd and B Pty Ltd are incorporated in Australia.

B Pty Ltd has 3 shareholders:

- Poli, who holds 30%

- Elena, who holds 30%

- Jason, who holds 40%.

Poli and Elena are both absentee individuals.

Together, they have an absentee controlling interest in B Pty Ltd as they have 60% of shares. That means B Pty Ltd is an absentee corporation.

B Pty Ltd has a controlling interest in XYZ Pty Ltd as it holds 55% of the shares. Therefore, XYZ Pty Ltd is also an absentee corporation.

Controlling interest exemption

An absentee person who holds a controlling interest in an absentee corporation may be eligible for an exemption such that they are taken not to hold an absentee controlling interest. If exemptions have been granted to all absentee persons who hold an absentee controlling interest, the absentee owner surcharge will not apply to the corporation.

The exemption may apply to corporations:

- which conduct a commercial operation in Australia

- whose commercial activities make a strong and positive contribution to the Victorian economy and community by using local labour, materials and services through an Australian-based entity

- which exhibit good corporate behaviour with a history of compliance with Australian laws.

The exemption does not apply to absentee corporations incorporated outside of Australia, or those with businesses like a landlord or property investor.

The Treasurer’s guidelines, published in the Government Gazette, explain how exemption decisions are made.

Before you apply, refer to the Treasurer’s guidelines issued on 1 October 2018 for the 2019 land tax year onwards. These guidelines include examples of how build-to-rent developments may qualify. The exemption ends when the development is completed, as the absentee owner will then be considered a passive investor or landlord.

Land tax groups

Absentee corporations may be part of a land tax group.

If all members of a land tax group are absentee corporations, the absentee owner surcharge applies to all land held by the members of the land tax group.

If only some members of a land tax group are absentee corporations, the absentee owner surcharge only applies to the land held by the absentee corporations.

All members of a land tax group are jointly liable for land tax owed by the group. That means we can recover land tax – including the surcharge – from any member of the group.

Example - land tax group

Company A, Company B and Company C are part of a land tax group. Company A is an absentee corporation.

The 3 companies own the following taxable land as at 31 December:

- Company A $1,000,000

- Company B $500,000

- Company C $500,000.

The total taxable value of land held by the land tax group is $2,000,000.

To calculate land tax:

- Work out land tax at the general rate on the total taxable value of land held by the group, i.e. $11,850 + (($2,000,000 – $1,800,000) × 1.65%)) = $15,150.

- Work out the absentee owner surcharge on the taxable value of land owned by the absentee corporation, i.e. $1,000,000 × 4% = $40,000.

- Add the amounts in Step 1 and Step 2, i.e. $15,150 + $40,000 = $55,150.

All members of the group are liable for the surcharge amount.

Notify us

If you are an absentee corporation that owns taxable land on 31 December, you must notify us by 15 January of the following year.

You can also tell us about any change to your absentee owner status by updating your details in our absentee owner notification portal.